MiCA Stablecoin Rules: What EU Enforcement Means for Stablecoin Payroll in 2026

The EU’s Markets in Crypto-Assets Regulation is no longer a forthcoming framework. It is an operational reality. For companies running stablecoin payroll for EOR workers in EU member states, MiCA has direct and practical implications. This article explains the MiCA stablecoin framework as it stands in 2026, what it means for EOR payroll programs, and what your team needs to know to stay on the right side of it.

.avif)

TL;DR

- MiCA (Regulation (EU) 2023/1114) is in force and has applied in phases. Rules for Asset-Referenced Tokens (ARTs) and E-Money Tokens (EMTs) applied from June 30, 2024. The remaining MiCA framework, including CASP rules, applied from December 30, 2024. Transitional arrangements for some Crypto-Asset Service Providers (CASPs) have been running through 2025 and 2026 in certain member states and are now closing.

- Under MiCA, fiat-pegged stablecoins like USDC are classified as E-Money Tokens (EMTs). Only authorized credit institutions or electronic money institutions may issue them for use in the EU.

- Circle received authorization from French regulators as an electronic money institution in 2024, making USDC and EURC among the first MiCA-aligned stablecoins available in the EU.

- USDT is not MiCA-compliant. As enforcement tightened, USDT availability has been restricted for many EU users across major exchanges and platforms. For EU EOR payroll programs, USDT is not a viable default stablecoin under the current regulatory environment.

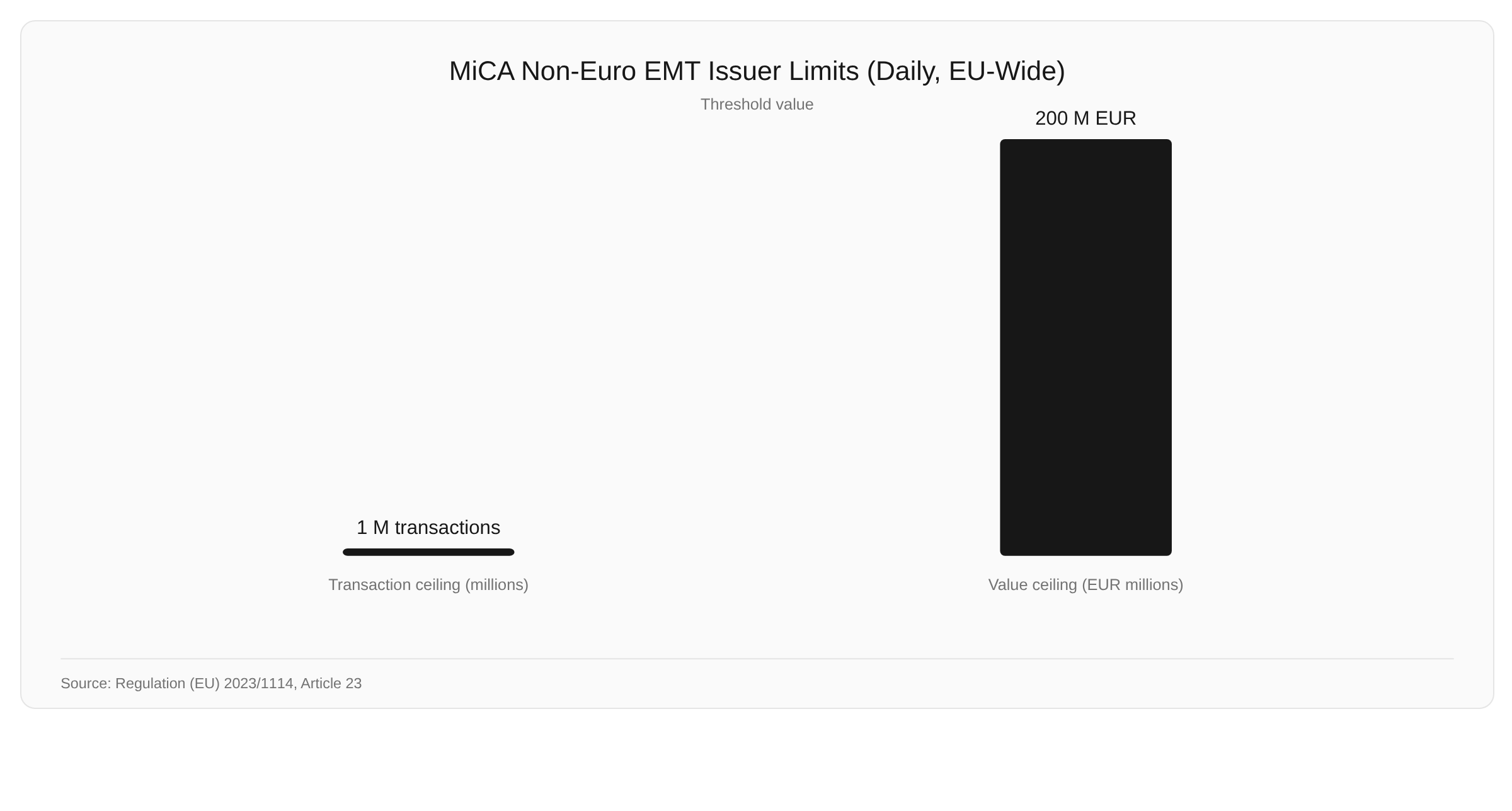

- MiCA includes issuer-side limits for non-euro currency EMTs used as means of exchange in the EU: 1 million transactions or EUR 200 million in daily value. This affects USD-denominated stablecoins such as USDC when used as a payment instrument at scale.

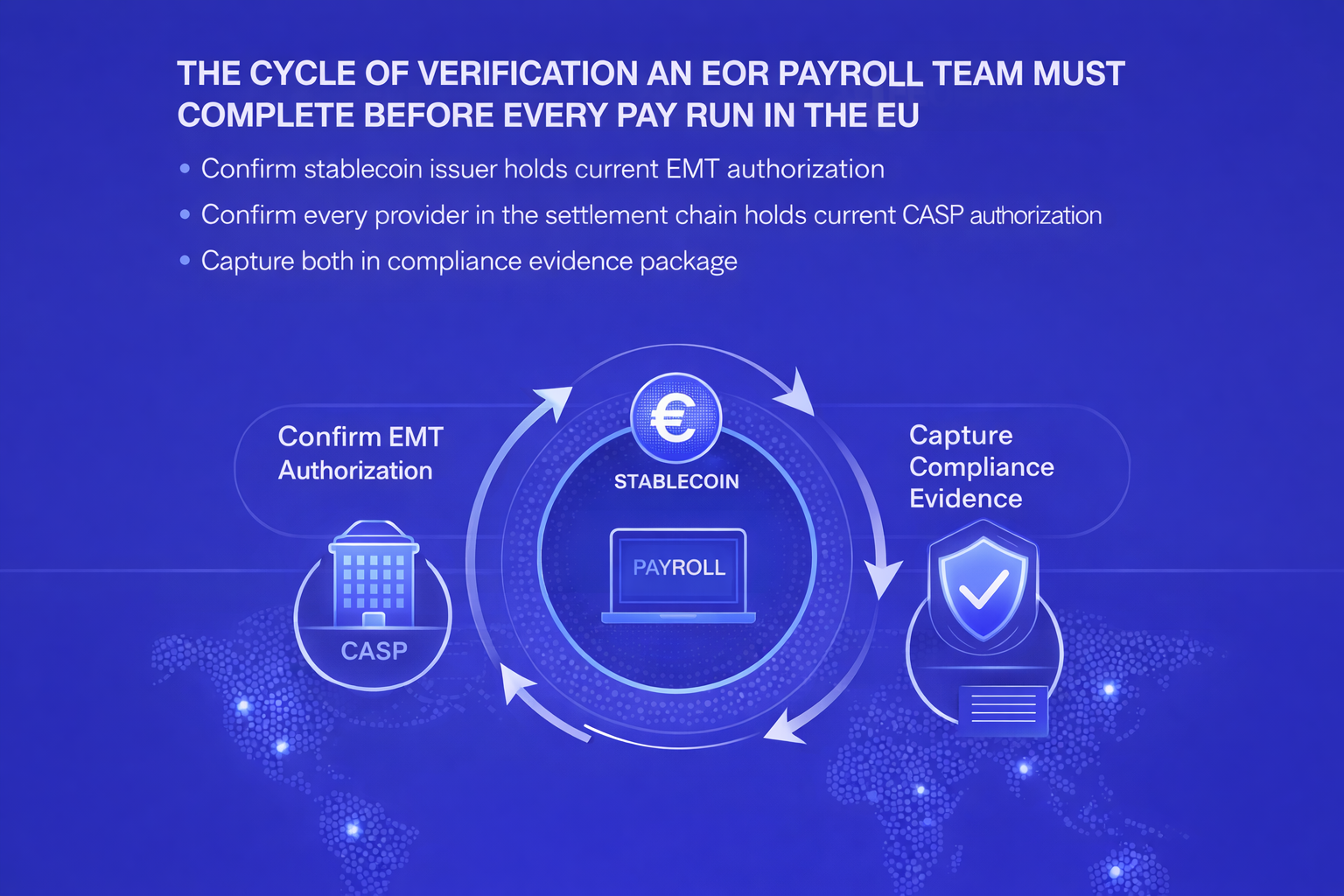

- MiCA does not directly regulate employers paying wages. Its obligations fall on stablecoin issuers and crypto-asset service providers. In practice, that means EOR payroll teams must verify that their stablecoin issuer and settlement providers are MiCA-compliant, and document that verification per cycle as part of the compliance evidence package.

Disclaimer: This guide is for general informational and educational purposes only. It does not constitute legal, tax, financial, or compliance advice. MiCA implementation and enforcement is active and evolving. Always confirm current regulatory requirements with qualified legal counsel for your specific jurisdictions and program structure.

Direct answer

MiCA’s stablecoin framework matters for EOR payroll programs in the EU because it determines which stablecoins are legally permissible for use as payment instruments in EU member states, and which providers can offer custody and settlement services for those stablecoins. The regulation does not impose obligations directly on employers paying wages. It imposes them on stablecoin issuers and crypto-asset service providers.

For payroll teams, this means the compliance question is not “do we need a MiCA license?” It is “are the stablecoins and providers we use MiCA-compliant, and can we document that compliance as part of our per-cycle evidence package?” In practice, that means verifying both the issuer’s EMT authorization status and the CASP’s authorization status for the services you rely on, including custody, transfer, and conversion.

What MiCA is and where it stands in 2026

MiCA, officially Regulation (EU) 2023/1114, is the EU’s comprehensive regulatory framework for crypto-assets and crypto-asset service providers. It was published in the Official Journal of the EU on June 9, 2023 and entered into force on June 29, 2023. Its implementation rolled out in two phases.

The first phase, covering stablecoin issuers specifically, applied from June 30, 2024. This brought E-Money Tokens and Asset-Referenced Tokens under a defined authorization and supervision regime for the first time across all 27 EU member states.

The second phase, covering all remaining MiCA provisions including the licensing requirements for Crypto-Asset Service Providers, applied from December 30, 2024. A transitional period allows CASPs that were operating under national law before December 30, 2024 to continue operating while seeking MiCA authorization, with the longest transitional window in many jurisdictions running until July 1, 2026. Some member states implemented shorter transitional windows, including the Netherlands at July 1, 2025 and Italy, Germany, and Austria later in 2025.

By mid-2026, the transitional period is closing across the EU. In member states using the longest transitional window, July 1, 2026 is the key deadline. After the applicable transition window ends, CASPs operating in that jurisdiction require MiCA authorization to continue lawfully.

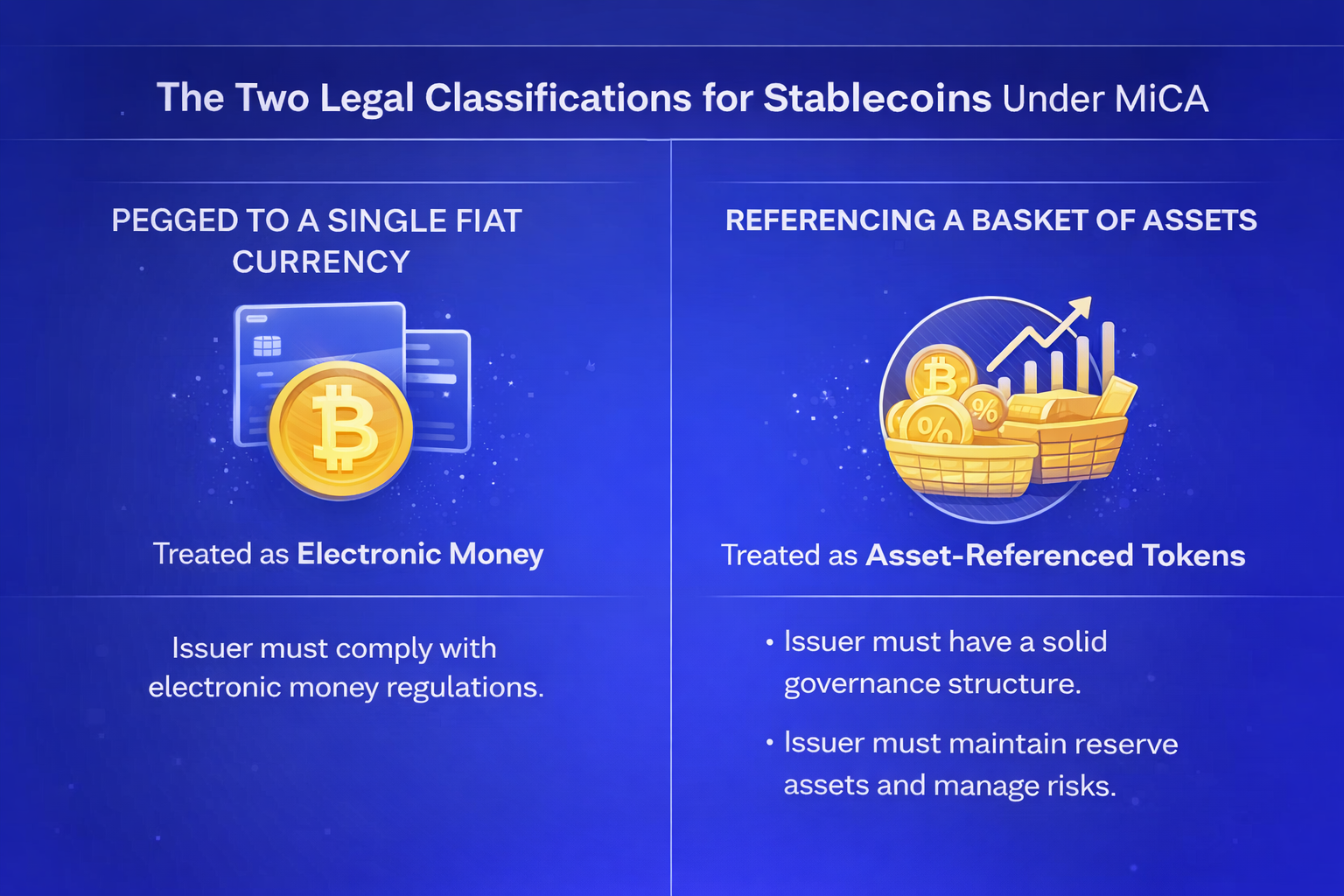

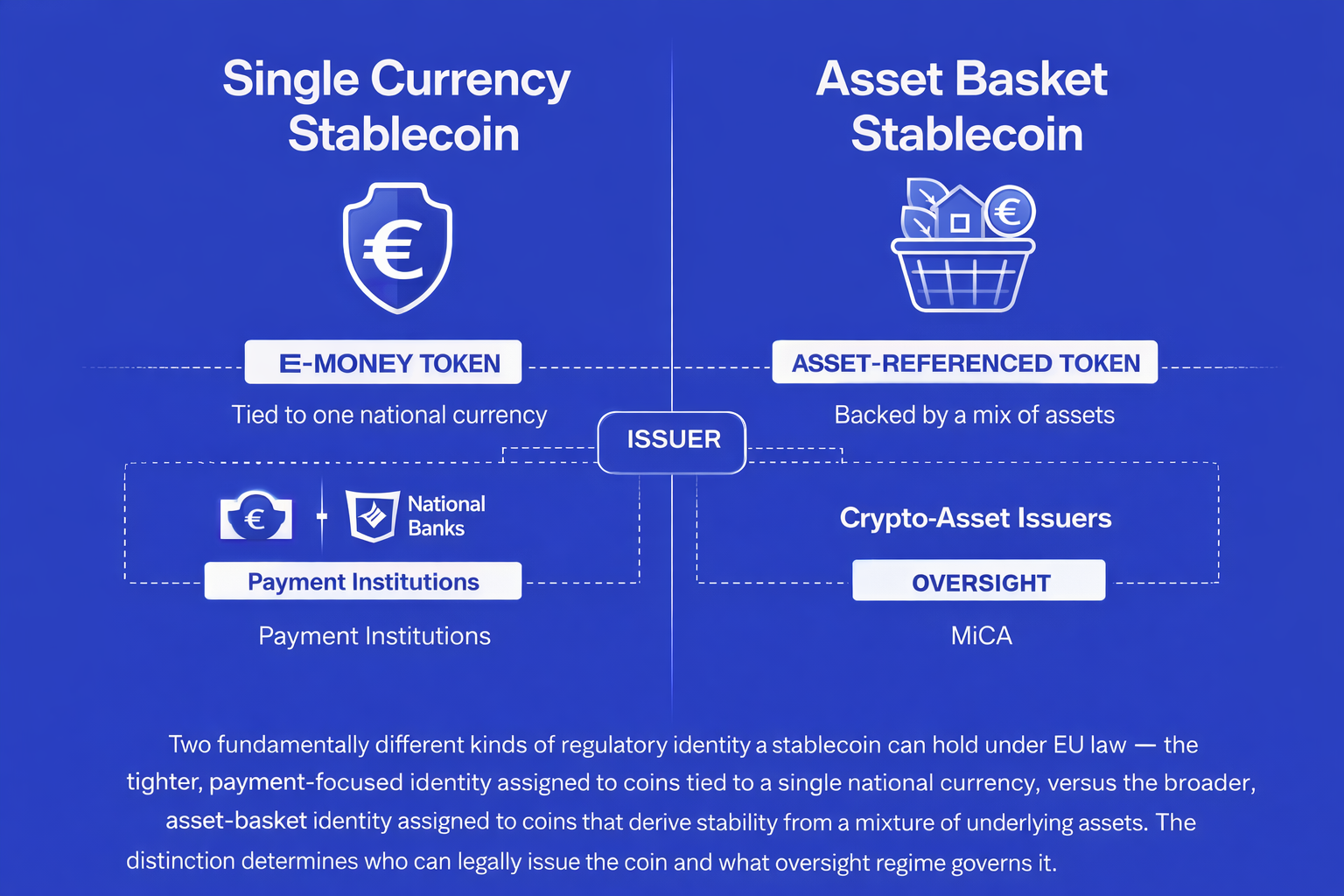

How MiCA classifies stablecoins

MiCA replaces the informal market category of “stablecoin” with two defined legal categories, each with its own issuer requirements, supervision regime, and operational constraints.

E-Money Tokens (EMTs) are crypto-assets that are pegged 1:1 to a single fiat currency and function primarily as a means of payment. USDC, pegged to the USD, falls into this category. EURC, pegged to the euro, also falls into this category. Under MiCA, EMTs are treated as electronic money. This means their issuers must be authorized as credit institutions or electronic money institutions. EMT issuers are subject to oversight by the European Banking Authority (EBA) for significant tokens, and by national competent authorities for smaller issuers.

Asset-Referenced Tokens (ARTs) are crypto-assets that maintain value by referencing a basket of currencies, commodities, or other assets rather than a single fiat currency. ARTs are not currently a practical stablecoin option for EU payroll programs, and the authorized issuer landscape remains limited.

For EOR payroll purposes, the relevant category is EMTs. The stablecoins payroll programs most commonly use (single-currency, redeemable at par) typically meet the EMT definition under MiCA. That means their issuers need EMT authorization to operate in the EU.

Which stablecoins are MiCA-compliant in 2026

The practical stablecoin landscape for EU payroll programs in 2026 has been reshaped by MiCA enforcement.

Circle’s USDC and EURC are among the most significant MiCA-aligned stablecoins available in the EU. Circle received authorization as an electronic money institution from French regulators (ACPR) in 2024. USDC and EURC are issued and operated under that authorization and associated MiCA requirements, including reserve, redemption, and governance obligations.

Tether’s USDT is not MiCA-compliant. As MiCA enforcement tightened, USDT availability has been restricted for many EU users across major exchanges and platforms. For EOR payroll programs in EU jurisdictions, USDT is not a viable default stablecoin under the current regulatory environment.

Other stablecoins may have obtained authorization or may be in the process of obtaining it. Because the market is actively developing, payroll programs should verify issuer authorization through official registers rather than relying on secondary sources or provider self-reporting.

The transaction limits: what they mean for USD-denominated stablecoin payroll

MiCA includes a specific issuer-side constraint on non-euro currency EMTs used as means of exchange within the EU. Under MiCA, issuers of non-euro denominated EMTs that are used as means of exchange must stop issuing new tokens once daily transactions exceed either 1 million transactions or EUR 200 million in total value across the EU.

This provision was designed to protect the euro’s role as the primary currency of the EU payment system and to prevent USD-denominated stablecoins from becoming de facto payment instruments that could undermine EU monetary policy. Its practical effect is that the issuer faces a ceiling on non-euro stablecoin payment activity, which creates incentives for euro-denominated alternatives in certain EU payment use cases.

For EOR payroll programs, the implication is nuanced. The limit applies to the issuer’s issuance obligations, not directly to individual employer payments. A payroll program paying EU-based EOR workers in USDC is not itself violating the threshold. However, if usage across the EU reaches the threshold, the issuer faces issuance constraints that can affect token availability and settlement reliability. This is a systemic risk that payroll programs operating at scale in EU markets should monitor. It is also one reason why programs with significant EU EOR workforces are evaluating EURC for EU-based workers rather than relying solely on USDC.

What MiCA means operationally for EOR payroll programs

MiCA’s direct obligations fall on stablecoin issuers and CASPs, not on employers. But it creates practical requirements for EOR payroll programs operating in EU member states.

Stablecoin selection and verification

Using a non-MiCA-compliant stablecoin to pay EU-based EOR workers creates compliance exposure. The stablecoin must be issued by an authorized electronic money institution or credit institution under MiCA. Before activating stablecoin payroll for any EU jurisdiction, confirm the stablecoin’s current authorization status against official registers and document it.

Provider authorization status

Any CASP involved in the settlement chain for EU payroll, including custody, transfer, or conversion, must hold MiCA authorization or be operating under a valid transitional arrangement for that jurisdiction. As the transitional period closes in 2025 and 2026, providers operating without authorization will have no legal basis to continue in the relevant member states. EOR payroll programs should confirm provider authorization status before each pay cycle runs in EU jurisdictions, and especially before reliance on any provider that has not completed authorization.

Reserve and redemption confidence

MiCA’s EMT framework includes reserve backing requirements, redemption at par, and regulatory reporting. For finance teams evaluating stablecoin payroll risk, MiCA provides a more formal structure for evaluating issuer soundness than existed before the regime applied.

EURC as an EU payroll stablecoin

For programs paying EU-based EOR workers, EURC avoids the issuer-side limits that apply to non-euro EMTs used as means of exchange, and it can eliminate a currency conversion step for workers in eurozone countries. Programs using USDC globally should assess whether EURC is more appropriate for the EU-based portion of the workforce.

Record keeping for MiCA-related due diligence

The compliance evidence package for EU payroll cycles should include confirmation of the stablecoin’s authorization status and the provider’s authorization status at the time of the cycle. This should not be treated as onboarding-only due diligence. Authorization status and provider operating posture can change, and documenting it per cycle creates a defensible record.

The July 2026 transition deadline: what changes

In member states using the longest transitional window, July 1, 2026 is the deadline for CASPs operating under national transitional provisions to either obtain MiCA authorization or cease operations. After the applicable transition window ends, the EU crypto-asset service landscape is governed by MiCA without the pre-existing national grandfathering pathway in that jurisdiction.

For companies evaluating international payroll platforms or global EOR providers for EU-based teams, this is a material vendor selection criterion. For EOR payroll programs, it matters in two ways:

1) Any provider relying on transitional arrangements that does not obtain authorization by the applicable deadline may not be able to continue lawfully, creating settlement disruption risk.

2) Post-transition, stablecoin options and provider availability are shaped by MiCA authorization status, which increases predictability but raises the importance of choosing compliant infrastructure before the window closes.

FAQs

Does MiCA require employers to obtain any license or authorization to pay workers in stablecoins?

No. MiCA’s licensing and authorization requirements apply to stablecoin issuers and crypto-asset service providers, not to employers paying wages. The employer’s obligation is to use stablecoins issued by authorized entities and process settlement through authorized providers, then retain due diligence evidence.

Is USDT still usable for EOR payroll in EU member states?

USDT is not MiCA-compliant, and its availability has been restricted for many EU users across major exchanges and platforms as enforcement tightened. Using USDT for payroll settlement in EU jurisdictions creates compliance exposure and settlement reliability risk. Programs operating in the EU should use MiCA-compliant stablecoins.

What is the difference between USDC and EURC for EU payroll purposes?

Both are issued by Circle under EU electronic money authorization and are compliant under MiCA’s EMT framework. USDC is USD-denominated and is subject to the issuer-side limits for non-euro EMTs used as means of exchange. EURC is euro-denominated, avoids that issuer-side constraint, and can eliminate currency conversion for workers in eurozone countries. For many EU-based EOR payroll use cases, EURC is increasingly the more operationally appropriate choice.

How do we confirm that a stablecoin or provider is currently MiCA-authorized?

Use official registers. ESMA maintains MiCA-related information and resources, and national competent authorities and the EBA provide issuer and authorization context. Programs should check registers directly rather than relying on secondary sources or provider claims.

Does MiCA affect how stablecoin wages are taxed for EU workers?

MiCA is a financial regulation, not a tax framework. It does not change the income tax treatment of wages paid in stablecoins, which remains governed by each EU member state’s domestic tax law and relevant EU directives. Confirm tax treatment with qualified tax advisors per jurisdiction.

What happens to our EU payroll program if our provider’s transitional authorization expires before July 2026?

If a provider’s transitional authorization expires in the relevant member state and the provider has not obtained MiCA authorization, the provider cannot legally continue providing crypto-asset services in that jurisdiction. Programs should monitor provider authorization status and maintain a contingency plan for provider transition before the applicable deadline.

Verify your stablecoin stack before the transition closes

MiCA has moved stablecoin regulation in the EU from a fragmented patchwork of national rules to a single enforceable framework. For EOR payroll programs, the practical consequence is the same: the stablecoins you use must be issued by authorized entities, the providers handling settlement must hold the appropriate authorization (or be within a valid transitional window), and both should be verified and documented before each pay cycle runs in EU jurisdictions.

The July 2026 transitional deadline is not the moment to start this assessment. In the jurisdictions using the longest transitional window, it is the moment it closes.

Related articles

Latest Case Study