Payroll Reconciliation for Global EOR Stablecoin Payouts: How Finance and HR Close the Books Cleanly

For finance and HR teams running EOR payroll across multiple countries, clean reconciliation after a stablecoin payout cycle depends on decisions made before the batch executes. This article lays out what “complete reconciliation” looks like in an EOR + stablecoin program, where reconciliation most commonly breaks down, and what teams need to produce to close the books with confidence.

.avif)

TL;DR

- Reconciling EOR stablecoin payroll means mapping each worker’s net pay on the approved payroll register to an approved payout instruction and a confirmed execution proof. If the chain can’t be traced end to end, the cycle isn’t reconciled in an audit-ready sense.

- Stablecoin payroll adds reconciliation inputs traditional payroll doesn’t: transaction identifiers, fiat-equivalent values at a defined conversion moment, network fees, and on-chain confirmation references.

- EOR adds complexity because gross-to-net, statutory deductions, and payslips sit with the EOR, while payout execution and proof capture may sit with a separate settlement layer (platform, treasury, or finance).

- Fiat-equivalent values should be captured at the defined conversion moment, not reconstructed later from blockchain data.

- Reconciliation is a per-cycle requirement, not a month-end exercise. Programs that defer reconciliation to close create more exceptions under more time pressure.

- Finance and HR have distinct but overlapping responsibilities. Defining ownership and the HR→Finance handoff before the first cycle prevents gaps and duplication.

Disclaimer: This guide is for general informational and educational purposes only. It does not constitute legal, tax, financial, or compliance advice. Payroll regulations and stablecoin rules vary by country and change frequently. Always confirm requirements with qualified legal counsel and payroll, tax, and compliance experts for your specific jurisdictions, entities, and worker types.

Direct answer

Reconciliation for global EOR stablecoin payouts means producing a complete, per-cycle evidence package that maps each worker’s approved net pay to (1) the approved payout instruction, (2) the executed stablecoin transaction (or alternative rail), and (3) confirmation proof - while documenting fiat-equivalent values at the program’s defined conversion moment.

For EOR programs, the reconciliation artifact must account for the split between:

- the EOR payroll layer (gross-to-net, statutory deductions, employer costs, payslip obligations), and

- the settlement/execution layer (payout execution, transaction proof, network fee reporting, and sometimes conversion reporting).

Finance is typically accountable for ensuring the reconciliation artifact exists, is complete, and is retained per cycle. HR owns the employment-side inputs that determine who should be paid, how, and under what elections. Both functions must align on timing, ownership, and what “closed” means before the first cycle runs.

Definition of “closed” (per cycle):

A cycle is closed when (1) the payroll register is approved, (2) payout instructions are generated from the approved register, (3) execution proof exists for each payout (or it is logged as an exception), (4) exceptions are resolved with approvals, and (5) the reconciliation artifact is finalized within a defined SLA (e.g., 2–5 business days).

Why reconciliation is harder in EOR stablecoin payroll than it looks

In domestic payroll, reconciliation is relatively contained: the payroll system produces a register, the bank executes transfers, and the bank statement confirms amounts. The chain is short and the data lives in one or two systems.

Global EOR stablecoin payroll breaks that simplicity in several directions at once. The EOR manages contracts, gross-to-net, statutory deductions, and payslip production - typically inside its own payroll system. Stablecoin payouts may be executed by the client company’s finance team, by a stablecoin payroll platform, or by the EOR (if it supports stablecoin settlement). Confirmation proof lives on-chain, in a provider dashboard, or both. Fiat-equivalent values need a defined policy and a captured record at a specific point in time. And across countries, some workers may receive fiat after conversion rather than direct stablecoin delivery.

No single component is inherently complicated. The challenge is that the data lives in different systems, is owned by different teams, and must be assembled into one coherent per-cycle artifact. Programs that don’t design the assembly process in advance end up doing it manually under month-end pressure, which is where exceptions multiply and audit readiness suffers.

Core terms (so the workflow stays consistent)

- Payroll register (approved): the source-of-truth record of gross-to-net results and net pay due per worker for the cycle.

- Payout instruction: the structured payout file/API payload generated from the approved register (amount, wallet/bank destination, rail, network).

- Conversion moment: the timestamp at which fiat-equivalent values are locked for documentation and reporting (defined by program policy).

- Execution proof: tx hash/provider reference + timestamp + delivered amount + fees (and conversion details where applicable).

- Reconciliation artifact: the mapping that ties register → instruction → execution proof, including exceptions and approvals.

Stage 0 (if applicable): Funding & prefunding record

Many stablecoin payroll programs involve treasury movements before payouts execute (for example: onramping fiat to stablecoin, moving funds into custody, or prefunding a payout wallet). If your program includes prefunding, retain a “Stage 0” record that covers:

- source account/wallet and destination wallet/custody account

- timestamps

- amounts (fiat and stablecoin)

- rate source and applied rate (if conversion occurred)

- fees and charges

This establishes provenance and prevents “where did these funds come from?” gaps during close.

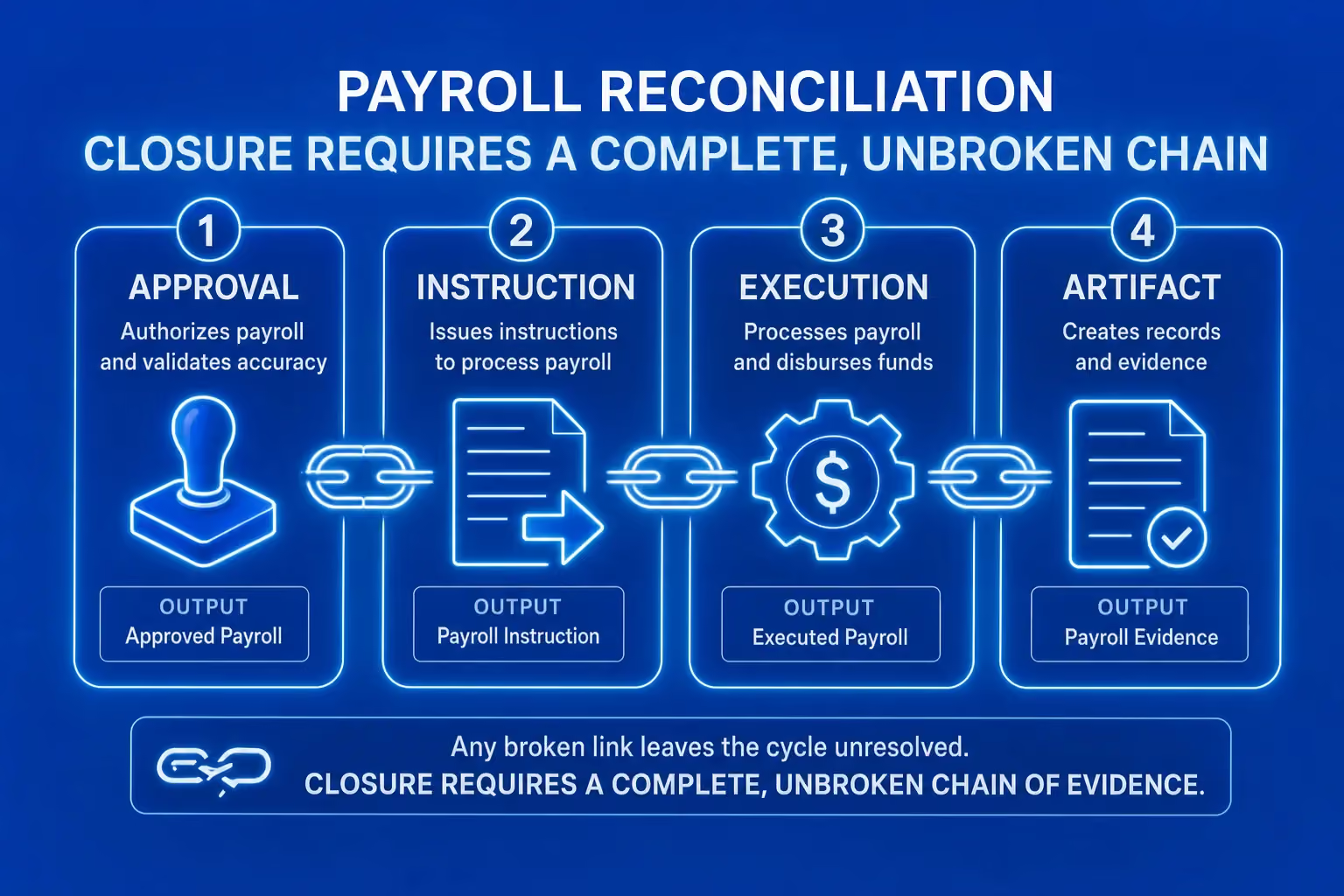

The reconciliation chain: what needs to map to what

A complete reconciliation traces a chain across four stages. Each stage has an owner and a specific output that feeds the next stage.

Stage 1: The approved payroll register

The EOR’s payroll platform (or the client company’s system of record, depending on program structure) produces an approved register showing each worker’s gross pay, statutory deductions, employer costs, and net pay due in fiat-equivalent terms.

This register must be formally approved (named approver + timestamp) before any payout instruction is generated. It is the source of truth for what each worker is owed. Every downstream reconciliation step maps back to it.

Stage 2: The payout instruction

From the approved register, generate a payout instruction for each worker that includes:

- net pay amount to settle (in stablecoin terms where applicable)

- destination wallet address (or bank account), plus network/rail

- fiat-equivalent value at the defined conversion moment (per policy)

The instruction should be generated directly from the approved register - not retyped - to eliminate transcription errors between what was approved and what was sent.

Stage 3: Execution proof

When payouts execute, capture for each payout:

- transaction identifier (tx hash) or provider confirmation reference

- execution timestamp

- stablecoin amount delivered (or fiat amount delivered if converted)

- fiat-equivalent value at the defined conversion moment (and/or at execution, depending on program policy)

- fees (network fees, platform fees, conversion fees if applicable)

- confirmation status (confirmed/finalized, number of confirmations if relevant)

This is the execution layer of reconciliation. It confirms that what was instructed actually happened.

Stage 4: The reconciliation artifact

The artifact maps Stage 1 (approved net pay) → Stage 2 (instruction) → Stage 3 (execution proof). Any mismatch between stages is an exception that must be documented and resolved.

If any stage is incomplete or undocumented, the cycle may have “paid out,” but it isn’t reconciled in an audit-ready sense.

Where EOR programs typically break down in reconciliation

Understanding failure modes lets teams design around them rather than discover them mid-cycle.

The register and payout instruction aren’t directly linked

When the EOR register lives in one system and the stablecoin batch is prepared manually in another, transcription risk appears immediately: wrong net pay, wrong wallet address, wrong network, missing/extra worker. These become exceptions that take time to identify and resolve.

Fiat-equivalent values aren’t captured at the right time

Teams capture the stablecoin amount and tx hash, but not the fiat-equivalent value at the conversion moment. When finance, tax, or auditors need the fiat value later, it gets reconstructed from historical rates - slow, error-prone, and difficult to defend. Capturing fiat-equivalent values as part of execution (or immediately at the defined conversion moment) avoids this.

Fees aren’t separated from principal

In stablecoin payouts, the “net pay” (principal) and fees (network/platform/conversion) can be handled multiple ways. If fees reduce what the worker receives (instead of being funded separately), the delivered amount may differ from the approved net pay. That creates systematic reconciliation deltas that must be explained.

A clear fee policy - documented, consistent, and reflected in the artifact - prevents this from becoming a recurring close problem.

Multi-currency programs lack a consistent conversion policy

If different corridors use different conversion moments or rate sources, reconciliation becomes harder to aggregate and harder to defend. Consistent conversion policies (or clearly documented corridor-specific exceptions) make reconciliation reviewable.

Exception resolution is undocumented

Failures, retries, and fallbacks happen in every payroll program. In stablecoin payroll, exceptions can be more complex: retries may execute on a different date with a different fiat-equivalent value, or the program may fall back to fiat rails. Exception notes (what happened, what changed, who approved) must live inside the reconciliation artifact - not only in tickets or chat.

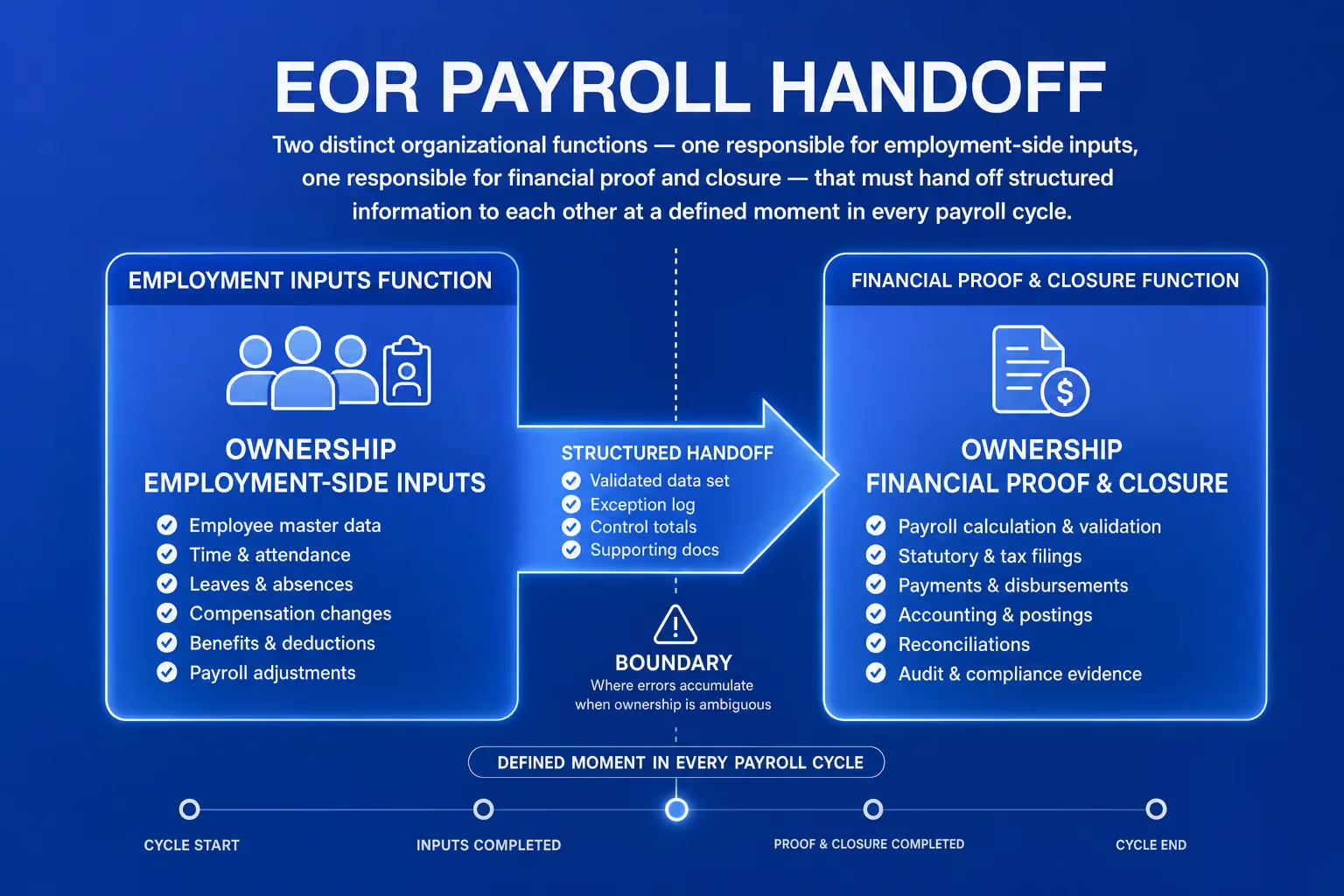

Finance and HR reconciliation responsibilities: who owns what

Reconciliation is a shared responsibility. The division of ownership matters.

Finance (accountable for closure)

Finance is typically accountable for ensuring the reconciliation artifact is produced and retained per cycle. In practice, finance owns:

- the reconciliation mapping (register → instruction → execution proof)

- exception log and resolution approvals

- fiat-equivalent documentation and conversion policy evidence

- fee accounting (principal vs fees; employer-borne vs deducted)

- retention, retrieval, and audit response readiness

HR (owns employment-side inputs)

HR owns the employment-side inputs reconciliation depends on:

- worker eligibility and status changes

- opt-in/opt-out status and payout split elections

- destination data governance (wallet/bank updates routed through controlled processes)

- payslip generation/distribution compliance (through the EOR, but tracked by HR for program integrity)

- change log of worker updates between cycles (so the register reflects the current population)

The HR → Finance handoff (where gaps form)

The handoff is where reconciliation usually fails:

- A worker opts out between cycles but the register isn’t updated before payout → HR input failure becomes a finance exception.

- A payout executes correctly but payslip net pay is wrong → finance proof is fine, HR escalations follow.

Define what HR provides to finance, by when, and in what format. Treat it as a cycle gate, not an informal “FYI.”

What a clean per-cycle reconciliation artifact contains

A reconciliation artifact that holds up in audit or finance queries should include, per cycle:

- Approved payroll register (with approver + timestamp)

- Payout instruction output generated from the register (amounts, destinations, rails/networks, fiat-equivalent values per policy)

- Execution proof report (tx hashes/provider references, timestamps, delivered amounts, confirmation status, fees)

- Reconciliation table mapping each worker’s net pay register entry → instruction → execution proof, with variances flagged

- Exception log covering failed payouts, retries, corrections, conversions, fallbacks, and manual interventions (with approvals)

- Fees and charges ledger separating principal (net pay) from network/platform/conversion fees, plus fee policy evidence

- HR sign-off confirming eligibility/elections were current and payslips were handled as required

- Conversion documentation (conversion moment definition, rate source, and how it was applied)

The artifact does not need to be one file. Many programs store exports (EOR register, provider payout report, treasury report) plus a summary mapping that ties them together. What matters is that the components are retrievable as a set and traceable end-to-end by someone who didn’t build them.

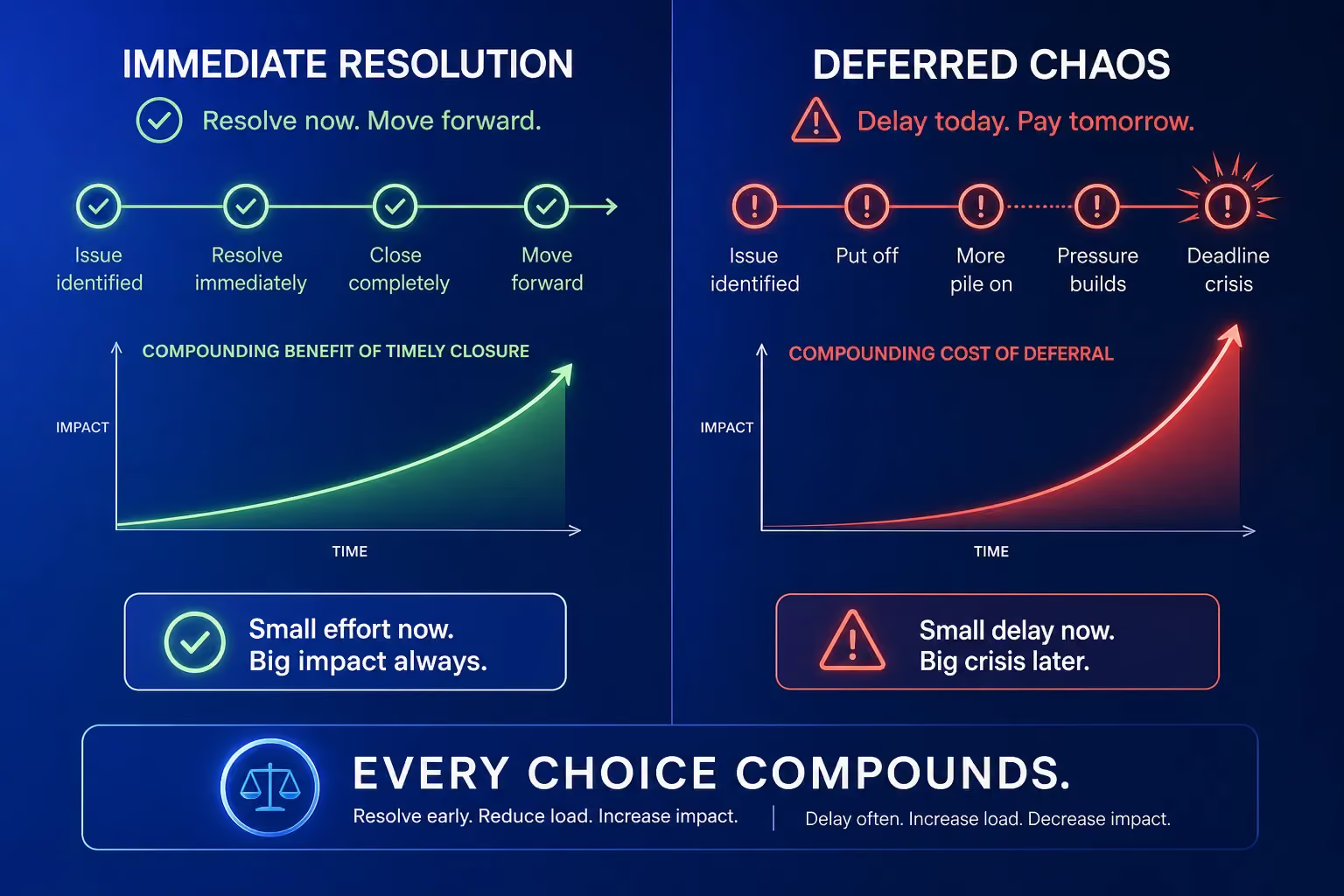

Reconciliation timing: per-cycle, not month-end

One of the most reliable improvements teams report after systematizing stablecoin payroll reconciliation is shifting from month-end reconstruction to per-cycle closure.

Per-cycle reconciliation means the artifact is completed and signed off within a defined number of business days after the batch executes. For programs with two payroll cycles per month, that means two closures per month - not one month-end fire drill trying to reconstruct two cycles at once.

Month-end close still happens, but with per-cycle reconciliation done, close becomes aggregation - rather than exception archaeology.

FAQs

Who is responsible for reconciliation in an EOR stablecoin payroll program: the EOR or the client company?

It depends on the program structure and provider capabilities. In many implementations:

- the EOR owns the payroll register, gross-to-net accuracy, statutory deductions, and payslips

- the client finance team (or stablecoin settlement layer) owns payout execution and the reconciliation artifact mapping approved net pay to executed payouts

Some EORs handle more of the execution layer if they offer integrated stablecoin settlement, but the client company should still confirm what reconciliation outputs the provider produces and whether they meet evidence requirements.

What is the best way to capture fiat-equivalent values at execution without manual intervention?

The most reliable approach is using a stablecoin payroll platform that captures fiat-equivalent values automatically at the defined conversion moment and includes them in payout confirmations. If not available, define the conversion moment precisely (e.g., batch release timestamp), pull the reference rate from a consistent source at that time, and apply it immediately across the batch. Reconstructing fiat equivalents later is a last resort.

How should we handle a payout that executed but the transaction reference wasn’t captured in time?

Most providers retain transaction records. Retrieve the reference as soon as possible after cycle execution and log it as an exception with a note explaining the capture gap. It’s usually not catastrophic, but it is a workflow defect that should be corrected.

Does each EOR jurisdiction need a separate reconciliation artifact?

Not necessarily. However, the artifact should be structured so jurisdiction-specific records can be extracted. Audit requests and tax queries are often country-specific, and a single consolidated artifact that can’t be segmented is less useful than one that can.

How do stablecoin payout failures affect reconciliation?

Each failed payout becomes an exception requiring: failure reason, resolution path (retry, fallback to fiat, hold), resolution timestamp, and approver. If a retry executes later, fiat-equivalent values may differ; capture and explain the delta. Reconciliation is not complete until exceptions are resolved and documented.

What should we retain, and for how long?

Retention requirements vary by jurisdiction. As a general principle, retain per-cycle reconciliation artifacts for at least as long as the longest applicable tax or employment record retention requirement across your in-scope jurisdictions. In practice, many teams plan for five to seven years. Store artifacts in formats that remain usable without specialized tooling.

Build reconciliation in before you need it

Reconciliation feels optional until it isn’t. The first audit request, tax query, or employee dispute that requires tracing a payout back to an approved register is when teams discover whether their reconciliation infrastructure is real or assumed.

Teams that close their books cleanly after every EOR stablecoin payout cycle aren’t doing more work than everyone else. They designed the workflow before the first cycle ran, defined ownership between finance and HR, and built fiat-equivalent capture and exception documentation into the operation from day one. That discipline pays for itself the first time something goes wrong - and the answer is already in the artifact.

Related articles

Latest Case Study